Choosing the business structure for your new venture is an important undertaking.

Many entrepreneurs form a corporation because of the liability protections and advantages for shareholders.

But compared to other business entities, corporations have the most regulated and complex structure—adding complexities to the incorporation process.

There’s a lot of paperwork to file, administrative tasks, and fees involved with getting started and maintaining a corporation.

This guide will teach you how to form a corporation, including a trick that will speed up the formation steps, making your life much easier.

The Easy Parts of Forming a Corporation

One of the biggest perceived hurdles of forming a corporation is the initial startup. Filling out forms and filing the correct paperwork with the appropriate state agencies—it’s an intimidating process for anyone, especially beginners.

Rather than paying a business attorney outrageous fees to walk you through this process, you can use an online incorporation service to get set up.

These services take the hassle out of forming a corporation, making the more difficult steps easier. They essentially walk you through a series of questions about you and your business. As you answer the questions, the service automatically fills out the appropriate paperwork and then files it with your state.

From choosing your tax structure to issuing shares and electing a board of directors, online incorporation services take you through each step of the formation process.

You can answer these questions from your computer, then just sit back and let the service handle the heavy lifting on your behalf.

There are lots of excellent business formation services on the market. But in terms of starting a corporation, LegalZoom is our top recommendation.

LegalZoom has been used to form over two million businesses, making it one of the most reputable and popular ways to start a new company.

LegalZoom has everything you need to succeed, whether you’re starting a C-corp, S-corp, or nonprofit corporation. The incorporation services start at just $149 plus state filing fees. If you’re not 100% satisfied with LegalZoom’s service, you can request a refund within 60 days.

Another reason why I like LegalZoom so much is that the services go beyond the basic incorporation process. They offer registered agent services and online attorney services so that you can get all of this under the same roof.

Using an online incorporation service ensures accuracy and timely filings with your state.

The Difficult Parts of Forming a Corporation

Not every aspect of starting a corporation is easy. Even if you’re using an online tool to simplify the process, you should still be aware of a few challenges.

Laws and regulations vary from state to state. But generally speaking, corporations have to follow stricter guidelines compared to other business entities. In short, this translates to lots of paperwork.

You’ll likely need to file annual reports, create corporate bylaws, hold meetings with your board of directors, and keep track of those meetings with corporate minutes.

The corporate entity structure can allow your business to go public, meaning you can issue shares on the stock exchange. While this is a great way to raise a significant investment from lots of outside investors, you’re also making these investors partial owners in the company.

It’s typically more expensive to set up a corporation than any other type of business entity. Sole proprietorships and LLCs are usually cheaper and easier to start.

The other challenge associated with forming a corporation is maintaining control. It can be tempting to issue shares either publicly or privately to raise money. But this also could limit your authority in making decisions.

Certain decisions need to pass through the board of directors for approval, and shareholders will have voting rights. Some entrepreneurs end up relinquishing control of their corporations without realizing what they’re doing.

Step 1 – Choose a Business Name

For this tutorial, I’m going to walk you through each step using LegalZoom. But the steps will look fairly similar no matter which online incorporation service you use.

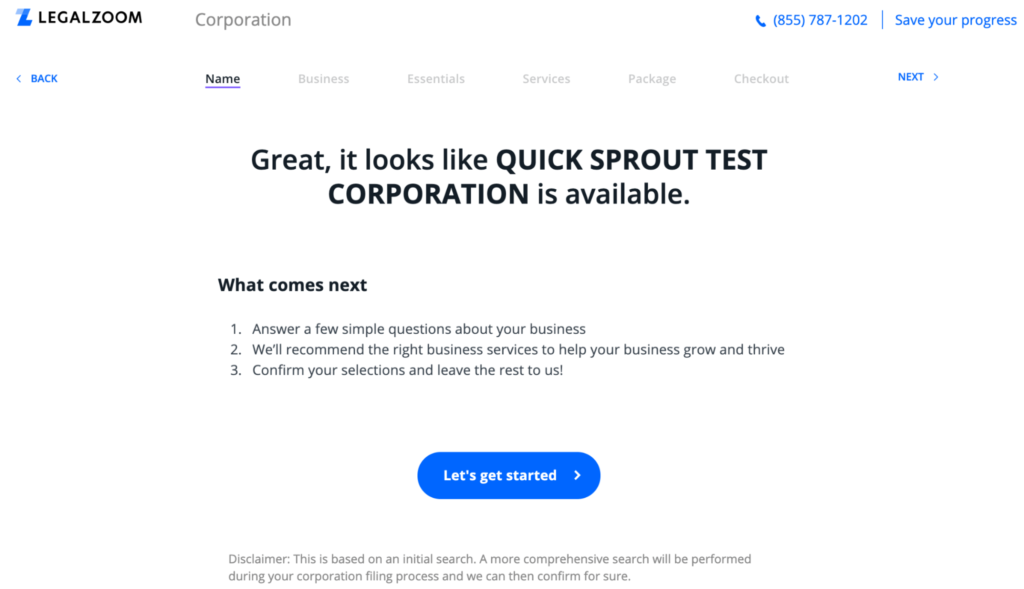

The first thing you need to do is pick a name. In addition to the name being brandable, it must be legally available. You’ll need to check with your state’s office to see if another corporation in your state has already registered that name.

One of the benefits of using an online incorporation service to get started is that you can run a name search directly through that platform.

I quickly ran a search for “Quick Sprout Test Corporation” in the state of California, and LegalZoom immediately told me that the name was available.

If you haven’t landed on a name just yet, you can skip this step and begin answering other questions to get the ball rolling. But you’ll need to have a name before you make anything official.

For those struggling to think of a name, check out our top tips for naming your startup.

Your corporation’s name won’t be legally registered until you officially file your articles of incorporation. But you might be able to reserve that name until the paperwork is filed. Just check with your state’s corporation office.

Register a DBA (Optional)

Some businesses plan to operate under a different name than the legal name of their incorporation.

If you fall into this category, you’ll also need to register a DBA (doing business as) name. This is also referred to as a fictitious name, assumed name, or trade name.

For example, “Quick Sprout Test Corporation” isn’t very brandable or marketable. In this case, registering a DBA as just “Quick Sprout” could be a better alternative.

DBA rules and regulations vary from state to state. There are even some city, county, and other local mandates surrounding DBAs. So check your local regulations before proceeding with a DBA.

Provide Additional Information About the Business

After you verify the availability of your business name, LegalZoom will get some quick preliminary details about your business.

- Business industry (technology, travel, consulting, restaurant, etc.)

- Are you a licensed professional service? (dentistry, law, medicine, etc.)

- Will your corporation hire employees in the first year?

- Tax status information

- Primary contact person for the business

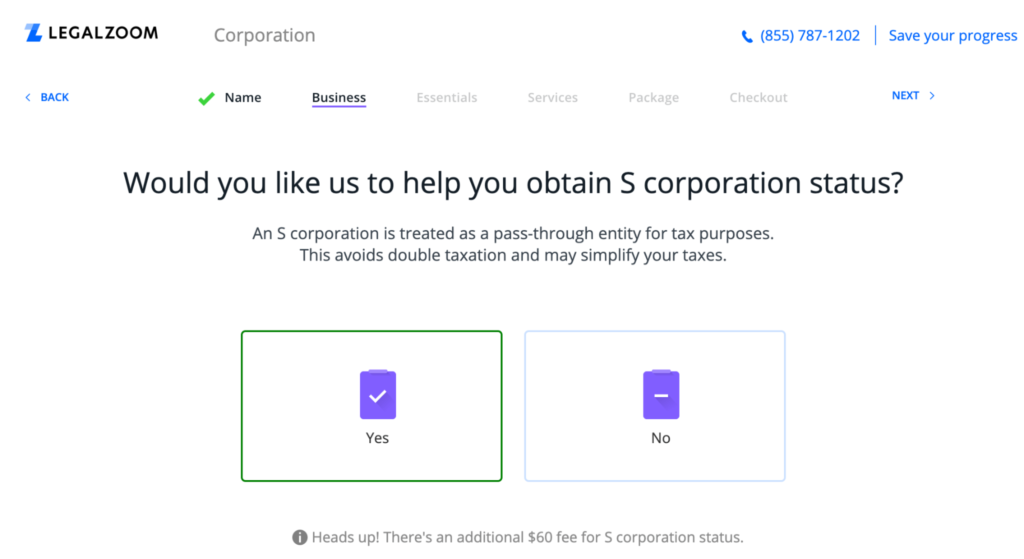

Some of these answers come with additional fees. For example, it costs more if you’re offering licensed professional services or if you want LegalZoom to help you get set up for S-corp taxation.

Step 2 – Decide What Type of Corporation You’re Forming

Within the blanket term “corporation,” there are a few specific entities that you can choose from.

- S Corporation

- C Corporation

- Nonprofit

Most of you will be deciding between S-Corp and C-Corp. But we’ll cover a quick overview of each option below.

S Corp

The most significant benefit of S-corp status is taxation. This type of corporation lets owners pass income, deductions, losses, and tax credits to shareholders without the obligation of federal corporate taxes.

Technically speaking, an S-corp isn’t a legal entity—it’s a federal tax status. Even though S-corps aren’t taxed at the corporate level, owners must pay taxes on their personal returns.

S corporations are better for smaller businesses that don’t want to go public. You can’t have more than 100 shareholders with this tax status, and you can only issue a single class of stock. Each shareholder in an S corporation must have equal voting rights.

It’s worth noting that you can always start a C-corp and apply for S-corp status at a later time. But many business owners know from the beginning what they want and decide to go with S corp status out of the gate.

C Corp

Forming a C corporation is more common for larger organizations. C corps are subject to double taxation, meaning the business itself is taxed, and the owners receiving profits also pay taxes on their personal returns.

While the taxation of a C-corp might be a turn-off for some people, there are actually many benefits to starting one.

Owner and investor liability is only limited to the amount of their capital investments. It’s also easier to scale by raising money from outside investors. If your main goal is to be publicly traded, then a C corporation will be the right option for you.

Nonprofit

Nonprofit corporations are tax-exempt in the eyes of the IRS.

This type of corporation does not have shareholders and doesn’t pay dividends. All of the profits made must be reinvested into the organization and used towards its charitable mission.

Many nonprofits are designated as 501(c)(3), meaning they are federally tax-exempt charities. This also means that donors can write off contributions made to the nonprofit corporation.

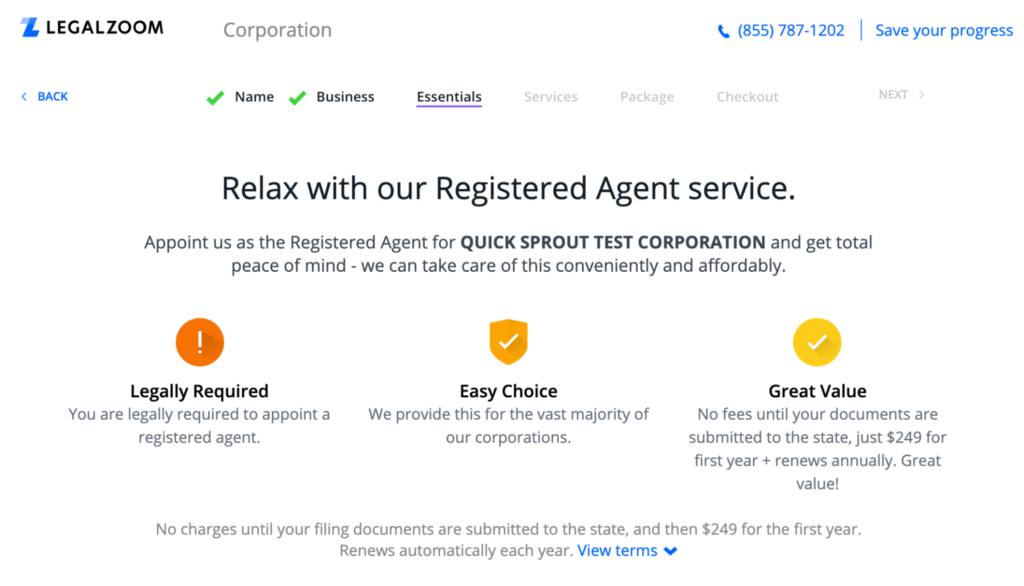

Step 3 – Choose a Registered Agent

Every corporation needs to appoint a registered agent with the state. Registered agents are also known as statutory agents, agents for service of process, or resident agents.

What is a registered agent?

In short, this can be an individual person or an entity that is legally appointed to receive government correspondence, compliance documents, and service of process on behalf of your corporation.

So if your corporation gets sued, the paperwork will be delivered to your registered agent.

Registered agents must be available in person during all regular business hours at a listed address. While you could technically be your own registered agent, we strongly advise against that.

Most online incorporation services also offer registered agent services.

LegalZoom lets you add this service to your formation package with a single click. So you can take care of this right now and never have to worry about it again.

Step 4 – Draft and File Your Articles of Incorporation

The articles of incorporation are the official paperwork that registers your corporation with the state. You could get these documents from the Secretary of State’s office and fill everything out on your own, but that’s a hassle you don’t need to deal with.

Instead, LegalZoom can handle the articles of incorporation and file them with the appropriate state agency on your behalf.

All you need to do is answer some questions about your business, and they’ll take care of the rest.

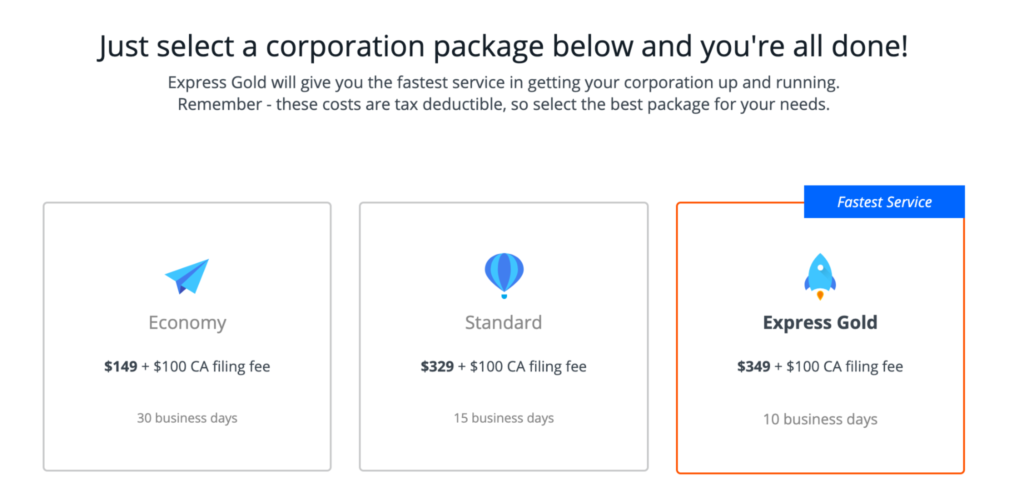

The filing time varies from state to state. You can also pay more to have LegalZoom expedite the process.

As you can see from the packages above, paying an additional $200 can get your articles of incorporation filed 20 days faster in the state of California. If you’re in a rush to get started and can’t wait one month, then I recommend going with the Express Gold package.

Obtain an EIN

In addition to registering your business with the Secretary of State, you’ll also need to register with the IRS, state, and any local tax agencies.

To do this, you need to obtain an EIN (employer identification number), also known as a tax ID.

You can get this number directly from the IRS. But it’s easier just to get it through your online incorporation service as you’re filing the articles of incorporation and going through the business formation process.

Draft Corporate Bylaws

Corporate bylaws define the governing rules for how your business will be run. The bylaws typically cover record keeping, issuing stock, meeting procedures, voting, and more.

While the corporate bylaws don’t need to be registered with your state when you file the articles of incorporation, it’s still one of the most important aspects of starting a corporation.

It is recommended to consult with a lawyer when drafting corporate bylaws to ensure everything is appropriately covered.

Draft a Shareholders Agreement

For stock-issuing corporations, you’ll need to create a shareholders agreement (also known as a stockholders agreement).

This document explains the legal rights of shareholders. It also covers the responsibilities and powers of the corporation’s management and its board of directors.

Most shareholder agreements contain:

- Rules for issuing new shares of stock

- Restrictions on transferring shares

- Share/percentage of ownership and valuation

- Guidelines that govern conflict of interest (like non-compete clauses)

- Dispute resolution

- How to handle when a shareholder dies or becomes incapacitated

The agreement should be legally drafted and issued to all shareholders.

Step 5 – Appoint a Board of Directors

The number of directors required on your board will be based on your state’s laws. Some states require corporations to appoint a minimum number of directors based on how many owners the company has.

It’s common for owners to appoint themselves on the board of directors. But it’s worth noting that not every director needs to be an owner.

Directors are responsible for appointing corporate officers, including the CEO, CFO, CMO, CTO, and other executive roles.

Hold a Board of Directors Meeting

The initial board of directors meeting after the articles of incorporation has been filed is extremely important. Not only will this meeting handle appointing officers, but it should cover a wide range of other topics that will get your corporation started.

For example, the initial board of directors meeting can dive into the taxation of your corporation.

As we mentioned, you can start as a C-corp and register for S-corp status later. This is something that can be discussed and voted on by the board of directors.

All meetings should be documented in your corporate minutes.

from Quick Sprout https://ift.tt/3iPe8Mo

via IFTTT

No comments:

Post a Comment